Do real estate agents conspire to drive up the price of real estate? A new class action lawsuit says they do. The lawsuit alleges the National Association of Realtors (NAR) and brokers are fixing prices by offering uniform commission rates to buyers’ agents. The NAR, however, denies any collusion, and does not regulate the price of real estate. Instead, it requires brokers and agents to offer buyers a uniform rate for their services.

Bait-and-switches

Many people complain about real estate agents and their bait-and-switch tactics, which appeal to the buyer’s fear of loss. The problem arises when the home advertised is actually off the market when the buyer calls the agent. In such cases, the listing has gone off-market as a result of «listing syndication gone wrong» or being «scraped» by an unauthorized website.

Another common example of bait-and-switch advertising is mortgages. In these schemes, real estate agents advertise very cheap apartments to lure potential clients and then tell them that the rates have risen. Once the customer visits the office, they discover that they were misled and must pay higher interest rates than advertised. They must convince the customer to sign up for the higher price. In the job market, recruiters use the same tactic. They advertise a cheap apartment with a low price, but when the client visits, the agent tells him that the apartment was sold and offers a higher price.

Another example of a bait-and-switch scheme is a limited-quantity offer. For example, a retail store owner may advertise a discount on a product, but then state that this offer is only available for the first ten customers. In this scenario, the seller is misrepresenting the true product or service. The seller is expecting a higher profit margin when the substitute product is inferior to the advertised one.

A bait-and-switch scam can be difficult to detect, but you should watch out for red flags. A sale that sounds too good to be true should be avoided — images of luxury apartments at rock-bottom prices are misleading and should be suspicious. Similarly, sellers should avoid using confusing fine print and stating that there is a limited supply of the product. So always read the fine print before making a purchase.

Anticompetitive restrictions

Whether or not anticompetitive restrictions on real estate prices are a problem is an open question, but there is evidence that anticompetitive restrictions have occurred in some states. These states have antitrust laws that limit competition, and a repeal of these laws would end these anticompetitive restrictions on real estate prices. Although the antitrust laws may seem unimportant, the effects they have on innovation and consumers could have important consequences for the real estate market.

Generally, any restraint on real estate prices that restricts competition is a violation of the Sherman Act. There are certain types of restraints that are illegal and are considered anticompetitive by the Supreme Court. Some of these restrictions are price fixing, group boycotts, market allocation, and customer allocation. The Federal Trade Commission (FTC) may also pursue such restraints. Moreover, the FTC may investigate the existence of anticompetitive restrictions.

The US real estate market is severely restricted by anticompetitive laws. Local cooperatives and other government agencies dominate the industry, and enforcing mandatory rules has hurt competition. The anticompetitive restrictions harm consumers by restricting the market and driving up prices. It also discourages competition by suppressing better ways of doing business. Anticompetitive restrictions on real estate prices should be rescinded.

Antitrust laws are important because they promote competition in the marketplace, which benefits consumers by keeping prices low and maintaining quality. This is especially important when real estate professionals are involved. While centralizing market information is helpful for buyers, policies limiting competition can affect consumers negatively. Antitrust laws are not intended to protect sellers, but they do protect buyers. If they do happen, antitrust laws should be a consideration in your real estate business.

Steering

While the impact of steering real estate agents isn’t always intentional, it is possible. For example, some brokers may show clients houses located in Latin communities, but without a clear intention to influence a client’s choice. Steering is a common practice among real estate agents, but recognizing the negative impact on competition may help avoid this practice. Below are some tips for dealing with real estate steering.

First, real estate agents shouldn’t steer buyers to communities that aren’t good for them. By influencing the decisions of potential buyers, agents are violating fair housing laws. These laws prohibit discrimination based on race, sex, and familial status. Whether or not real estate agents are steering based on these characteristics is unethical and illegal, but it’s a widespread practice in the real estate industry.

Steering agents is another example of unfair business practices. This practice discriminates against prospective buyers and only shows them homes in neighborhoods with high property values. This practice is illegal and unethical, and it violates the Fair Housing Act. In addition, it is considered racist. Regardless of the motivations, the practice of steering agents to drive up real estate prices has consequences that go beyond the ethics of the profession.

Fee structures

Buying and selling a home are major financial decisions, and can be costly. Most consumers don’t take into account all of the costs involved, including broker and agent fees. Getting a handle on these costs will help you make an informed decision when buying or selling a home. Here are three ways that fees and commissions from real estate agents drive up prices:

First, consider the traditional model. In the past, the same brokerage represented the buyer and the seller. That meant commissions were split. This model also increased the commissions if the house sold for more money. However, lawsuits forced this system to change. Today, the buyer’s agent is presumed to represent the interests of his client, and is paid a percentage of the sale price. Because of this, higher price tags mean higher commissions for buyer’s agents.

In the past, there was little information about the fees charged by buyer brokers. Today, consumer-facing real estate websites have more information than ever before, but they often fail to mention buyer agent fees. These fees are often hidden in the contract, and agents don’t dwell on them. As a result, buyers don’t understand why the buyer agent is paying so much. Some consumers think that a low-priced service means a lower price, which is not necessarily the case.

Service levels

Many people wonder if the service levels of real estate agents are driving up real estate prices. If so, this is a baffling question. The market for real estate services works similarly to most other service markets: consumers choose the level of service that is most appropriate for them from a menu of options. In a free market, consumers would be free to choose which service levels they want from among the list of real estate agents.

Minimum service requirements, on the other hand, limit consumer choice by forcing brokers to provide only the minimum services consumers require. Not only do these laws limit consumers’ choices, but they also reduce competition among brokers. Fee-for-service brokers can no longer compete with minimum service brokers. As a result, consumers end up paying for services they may not need. It also makes real estate agents look more expensive.

Some of the best predictors of real estate prices are the Stock market, Interest rates, Bidding wars, and Home inventory levels. However, there are several others that can also play a role. Listed below are some of them. Depending on your goals, you can even use some of them to make your own forecasts. But which ones do you need to watch? Hopefully, these tips will help you.

Interest rates

Rising interest rates have the potential to cause both a frenzy and a retraction in the housing market. It all depends on the condition of the market. If prices are high, interest rates will likely lead to a reduction in demand, which will lower the supply of homes on the market. Rising interest rates, on the other hand, will help multifamily investors as buyers will continue to rent their units while waiting for housing prices to come down.

Another reason that interest rates may have an impact on real estate prices is that mortgage application levels are at a high level. Mortgage applications remain well above their pre-COVID levels. These factors, combined with a low inventory of homes for sale, make interest rates some of the best predictors of real estate prices. This has created a perfect storm for low and no-interest mortgages.

Rising interest rates have impacted the affordability of home purchases, but the current economic situation makes that difficult. Home prices are already at record highs. While interest rates are affecting prices in the housing market, they do not affect salaries or wages. However, rising interest rates could also hurt the rental market. In such a scenario, it is better to buy now than wait for higher interest rates.

Stock market

Although there is no definitive forecast when it comes to the real estate market, there are some indicators that can help you understand when the time is right to invest in a home. The main barometer for the U.S. economy is the S&P500 index, which includes 500 blue-chip companies including housing related firms. Investors use the global stock markets to make their predictions on real estate. If they believe that the U.S. housing bubble is about to burst, they’ll start selling stocks in the real estate industry.

Similarly, a 10% — 15% stock market correction will make real estate prices increase and the stock markets fall. While this might be a good scenario for both investors, you’re better off predicting a 15% stock market correction, which would lead to maximum real estate outperformance. Investing at this time is beneficial because the market is more jittery than panicked investors, which will drive more money to real estate and stocks.

If you can forecast house prices ahead of time, you’ll be one step ahead of the curve and can sell your assets before the inevitable crash. Housing market crashes don’t happen overnight; they materialize over several months. As a tangible asset, property is highly illiquid, with a finite supply of buyers and sellers, it can take months for changes to be obvious. With that in mind, it’s crucial to make your real estate investments carefully before the market crash.

Bidding wars

When bidding wars occur, there’s a good chance the price of a home will increase. Prices have risen sharply this year because of a lack of inventory. The demand for homes has outstripped supply in many markets, and fewer homes on the market has meant heightened competition. While the national bidding war rate has cooled slightly, competition rates remain high in cities like Boston, San Jose, and Austin.

Homebuyers that win bidding wars tend to make the highest offer. However, the highest offer is not always the winning one. The seller’s decision often depends on the buyer’s payment method and terms of the purchase agreement. Buyers can use several strategies to beat their rivals’ offers. Some buyers will make multiple offers to maximize their chances of winning the property. This tactic can lead to bidding wars, even if the highest offer is not the one that gets accepted.

A bidder must have a realistic budget when buying a home. When submitting an offer, the buyer puts down an earnest money deposit, which is normally 1% to 3% of the price of the home. Putting down a larger earnest money deposit shows the seller that you’re serious about buying the property and willing to put more on the line for it. The downside of this tactic is that if the deal falls through, you’ll have less money available to pay for closing costs and other expenses.

Home inventory levels

According to Zillow, home inventory levels have decreased by almost 25 percent in February from February 2021. This is the fifth consecutive month that inventories have decreased. Many housing economists are now pointing to inventory as one of the most important indicators of real estate prices. Although little fluctuations in home inventory aren’t likely to affect a seller’s price, they do indicate a trend worth watching. If there is a steady increase in inventory, home prices may be headed higher.

In recent years, investors have been buying up homes, and this has caused a shortage of housing inventory. Low inventories have also exacerbated competition for traditional home buyers, and a lack of new home construction has contributed to this shortage. As a result, builders have struggled with unstable building supply costs and shortages of skilled tradespeople. New build permits are currently 24% behind schedule, and are not expected to recover until 2022.

While rising interest rates may create a «lock-in» effect for homeowners, they do have a positive impact on home prices. As a result, more sellers are likely to come onto the market. However, this doesn’t necessarily mean that home prices will rise, as affordability conditions aren’t necessarily in favor of more sellers. Currently, ninety-five percent of housing markets are less affordable than they were a decade ago. A recent survey conducted by Gallup showed that seventy percent of Americans think that this is the worst time to buy a home.

Interest rate hikes

While most property values are driven by inflation, real estate prices can also be affected by interest rates. If interest rates are raised, the market may retrace or go into frenzy, depending on the market conditions. A sharp rise in interest rates could mean fewer buyers for a particular property, which could ease the pressure on the real estate market. This can have both positive and negative effects on real estate prices.

Higher interest rates are scary news for new and cautious investors alike. The multifamily market is already bloated with Class A housing, which pushes cap rates down. Higher interest rates will further restrict cap rates for new property buyers, making real estate less appealing to short-term investors. Higher interest rates also affect the number of people who can qualify for a mortgage. For that reason, rising rates will slow the pace of real estate price growth.

The Federal Reserve’s recent interest rate hike will likely impact the housing market in the near future. In May, the Fed raised the federal funds rate. It’s expected to increase rates in each of the five remaining FOMC meetings this year. The action of the Fed directly impacts mortgage rates. A hike in the federal funds rate is a signal that the Federal Reserve is planning to raise rates and offset the historically high inflation. While the Fed’s actions don’t affect real estate prices directly, they indirectly affect mortgage rates. For instance, the 30-year fixed rate spiked by 17 basis points after the meeting in May. Another hike in the coming months is expected at the June 14-15 meeting.

Home price growth

Real estate prices are impacted by many factors other than supply and demand. For example, the average home size in the United States in 1950 was just 983 square feet. In 2015, the average home size reached 2,740 square feet, according to the National Association of Home Builders. In some parts of the country, the size of homes increased more than 10 times faster. That means that home prices will continue to grow, even in the middle-tier of price ranges.

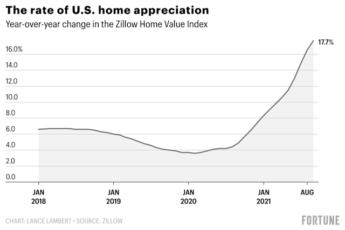

Zillow, a leading player in the real estate industry, predicts that the U.S. home price growth will grow 16.7% by the end of 2022, a gradual decline from 2022. Then, it predicts a slower growth rate in 2023, down to 5%. This slowdown may help avert a real estate market meltdown in 2023.

Mortgage rates are another major factor in real estate market performance. Increasing mortgage rates will drive up the cost of purchasing a home. If mortgage rates continue to rise, home prices will fall. A shortage of housing in some markets will push home prices higher. However, a lack of supply will result in elevated mortgage rates, reducing the number of homebuyers. This will affect the affordability of home prices.

Historically, home price growth has increased by almost one-third in the United States. However, after the Pandemic, this gap began to narrow. The rise in prices was partly due to larger homes and inflation. Home prices rose by 15.9 percent in 2021, and are expected to increase by only half that amount again in 2022. But this growth isn’t guaranteed, and the market will continue to remain a Seller’s market.